In the modern world, the calculation of greenhouse gas (GHG) emissions and carbon reporting in general are turning from a niche area into an important component of non-financial reporting in the functioning of a modern progressive company. Every year the number of reporting companies is steadily growing, as the results of calculations have a significant impact on their position in the market. Investors often prefer organizations that take into account their carbon footprint and take measures to reduce it. Pressure from governments and investors also encourages companies to conduct more transparent environmental reporting, take into account the impact of their own carbon footprint on the environment and pursue corporate policies in the field of sustainable development and ESG.

Reasons for accounting for GHG emissions:

To date, various GHG accounting standards have been formed, but the GHG protocol and the ISO 14064 standard are fundamental.

Let’s look at these two documents and compare them:

The developers of the GHG standard are the World Recourse Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). The GHG protocol emerged when these organizations recognized the need for an international standard for corporate accounting and reporting on greenhouse gases back in the late 90s. The first edition in 2001 was updated with additional guidance that explains how companies can measure emissions from energy purchases, as well as account for emissions throughout the supply chain.

The Protocol on Greenhouse Gas Emissions defines clear requirements for the structure and content of corporate carbon reports and for the set of key indicators contained therein. An important aspect of the Greenhouse Gas Protocol is the definition of scales, which distinguishes between different types of emissions and avoids double entries. The protocol helps to understand how to properly structure all sources of emissions and show what is included and what is not included in the assessment.

The GHG protocol contains a large number of guidelines on procedures and methods for calculating greenhouse gases. The protocol covers the calculation methodology for Scope 1 and 2, that is, the calculation of direct and indirect energy emissions. There is also a separate guide for calculating indirect greenhouse gas emissions, that is, emissions from the supply chain – Scope 3.

Intersectoral – designed for various enterprises and industries, regardless of their field of activity. At the moment, a free beta version of the Excel-based GHG emissions assessment tool has been developed.

For individual countries – the specifics of the environmental legislation of each state are taken into account.

Industry – developed for a specific service sector or production area.

For countries and cities – provides an opportunity to track global progress in achieving climate goals.

The Corporate Accounting and Reporting Standard contains requirements and recommendations for commercial companies and other organizations that prepare reports on greenhouse gas emissions at the corporate level. All seven GHGs of the Kyoto Protocol are taken into account – carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PCPs), sulfur hexafluoride (SF6) and nitrogen trifluoride (NF3).

The standard does not require the submission of information on emissions to the WRI or WBCSD and does not contain standards for the verification process, but only describing the sequence of work in assessing the organization’s emissions and preparing reports, provides step-by-step instructions and spreadsheets that help to calculate GHG emissions from specific sources or industries.

Allows companies to assess the impact of emissions and identify opportunities to reduce them throughout the product creation chain from the production of raw materials to finished goods.

Since these data are often not available and cannot be accurately determined, the Scope 3 calculation guide helps to understand which grip of emissions at different stages of the supply chain can be rational under conditions of uncertainty in the data. For example, emissions from the creation of production assets of technological equipment can also be taken into account when calculating emissions according to Scope 3, but due to insufficient information, they can be excluded from the assessment.

GHG Protocol Scope 3 is the most comprehensive and the only internationally recognized method of accounting for indirect emissions in 15 categories. With its help, almost all the reporting requirements for greenhouse gas emissions that a company must meet can be met.

The Product Lifecycle Accounting and Reporting Standard is used to calculate emissions from a product during its full lifecycle, including raw materials, production, transportation, storage, use and disposal, and focuses on maximizing GHG emission reductions in these processes. This creates a competitive advantage of the product, simplifies the development of responses to the environmental demand of consumers and is an important step towards more environmentally friendly products.

The World Resources Institute, C40 Cities Climate Leadership Group and Local Governments for Sustainability (ICLEI) have jointly developed a Global Protocol for Community–Scale Greenhouse Gas Emission Inventory (GPC), which in version 1.1 offers cities and local governments a reliable, transparent and globally accepted framework for consistent determination, calculation and reporting of GHG emissions in cities, demonstrating their important role in the fight against climate change.

It provides guidance on the development of national and subnational environmental mitigation goals and offers a standardized approach to assessing and reporting on progress towards achieving global goals in the fight against climate change.

The standard helps government agencies set emission reduction targets, meet domestic and international reporting obligations, and ensure that the intended results are achieved.

Emission reduction analytics at both the national and local levels assesses the impact of specific policy measures on GHG emissions, and provides recommendations for improving the effectiveness of measures taken, as well as indicates the direction of investment of resources to achieve the best results. Developed together with the aforementioned Mitigation Goals Standard.

The standard helps government agencies and other decision makers in the field of climate change to develop effective policy strategies for managing GHG emissions reduction and provides access to consistent and transparent public reporting on the effectiveness of the policy.

The GHG Emissions Protocol for Project Accounting is the most comprehensive and politically neutral tool for quantifying the benefits of climate change mitigation projects through emission reduction.

Any organization seeking to quantify the reduction of greenhouse gas emissions as a result of the implementation of certain projects can use the Project Protocol. However, it is not intended to be used as a mechanism for quantifying GHG emission reductions across a corporation or enterprise as a whole; the Corporate Standard mentioned at the beginning should be used for this purpose.

The International Standard for Corporate Reporting on Greenhouse Gas Emissions, which was first published in 2006 to create a greenhouse gas reporting standard that is fully compatible with the established ISO standards for energy and environmental management (ISO 14001 and 50001). In 2007, ISO, WBCSD and WRI also decided to jointly support the Greenhouse Gas Protocol and ISO 14064 (Memorandum of Understanding). ISO has standards that are related to the assessment of greenhouse gas emissions and reporting for this assessment for both products and organizations. The ISO 14064 series of greenhouse gas reporting standards was developed taking into account the experience of creating the GHG protocol.

Thus, ISO 14064 Part 1 complies with the GHG protocol for corporate reporting, and Part 2 complies with the GHG Protocol standard for projects to reduce greenhouse gas emissions.

Validation is the verification of the methods, conditions and assumptions that are used in conducting assessments.

Verification is the verification of calculation results, verification of the correctness of the source data used and identification of deficiencies in calculations and in the application of calculation methods.

The categories of greenhouse gas emissions at the organization level in accordance with the first part of ISO 14064 consist of the following 6 categories:

The difference between these two documents is that the GHG Protocol defines, clarifies and provides options for the best methods for calculating GHG, while ISO 14064 sets minimum standards for compliance with these methods. The GHG protocol simplifies the comparison of companies due to a more complete categorization of emissions according to Scope 3, which allows better comparison of indicators, as well as more targeted strategies for managing emissions and reducing emissions. Like the GHG protocol, ISO distinguishes between direct and indirect emissions, but does not define the scope of application. Scope 1 emissions in the Greenhouse Gas Protocol correspond to direct emissions of ISO 14064, but in ISO Scope 2 and 3 are summarized in indirect emissions. In addition, ISO 14064 does not contain strict guidelines for the categorization of indirect emissions and imposes other requirements on the structure and content of the report.

However, in fact, the emissions covered by both standards are almost identical. But despite this, both documents are complementary – ISO defines what to do, and GHG explains how to do it. Organizations conducting GHG emission assessments and seeking independent verification can benefit from using both the ISO standard and the GHG protocol as reference materials.

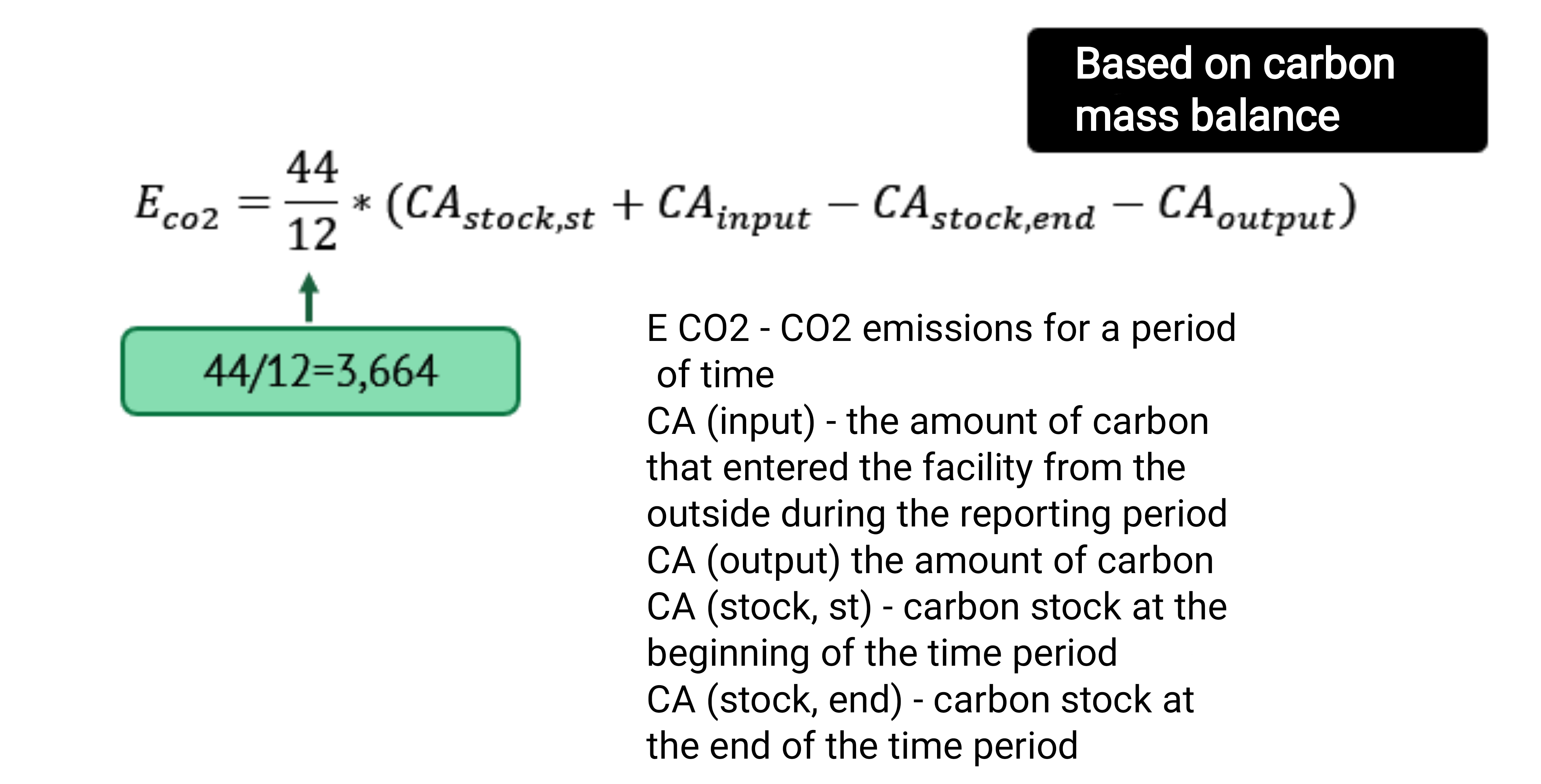

This method is used when it comes to technological processes. CO2 emissions depend on the volume of carbon-containing components at the inlet and outlet of the processes. The amount of emissions is calculated based on the balance at the inlet and outlet. For example, calcination of limestone, during which calcium carbonate decomposes into calcium oxide and carbon dioxide. When calculating CO2 emissions in the metallurgical process, it is necessary to use the mass of carbon at the outlet and the correction factor, which convert the molar mass of carbon into the molar mass of carbon dioxide.

The formula for calculating carbon dioxide emissions based on the mass balance of carbon:

It is known that the rounded molar mass of carbon dioxide is 44 g/mol, and carbon is 12 g/mol. That is, having data on the mass of carbon in tons at the inlet and outlet of the process, it is necessary to recalculate carbon into carbon dioxide emissions by multiplying the resulting mass of carbon by 44/12 or immediately by 3,664. Thus, tons of carbon are converted into tons of carbon dioxide by multiplying by this coefficient.

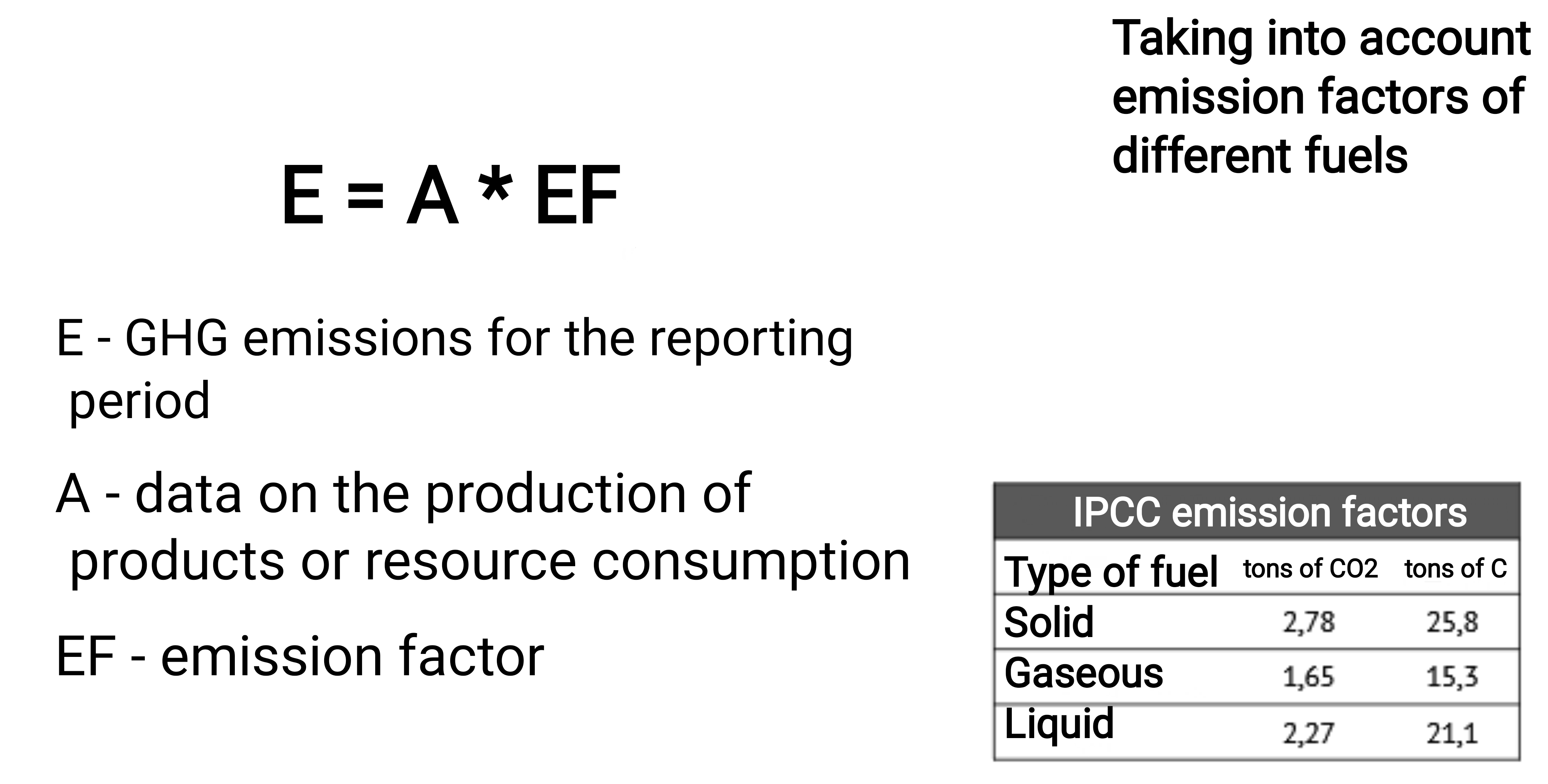

It is used to determine emissions from the fuel being burned, when combustion and emissions from combustion are calculated depending on the emission coefficients for each type of fuel. The initial data for this calculation is the amount of fuel burned and the type of activity of the organization.

To calculate greenhouse gas emissions using this method, it is necessary to understand the processes that produce emissions and the amount of fuel burned – the value A in the formula. Next, the emission factor EF (Emission Factor) is used. It is determined based on the carbon content of various fuels. The coefficient shows the amount of CO2 emissions depending on the amount of energy produced, that is, the unit of measurement is a ton of CO2/megajoule. To apply these emission coefficients, it is necessary to determine the energy equivalent of the fuel used according to the reference tables. The units of measurement in this case are the number of kilocalories per kilogram of fuel or megajoules per kilogram of fuel.

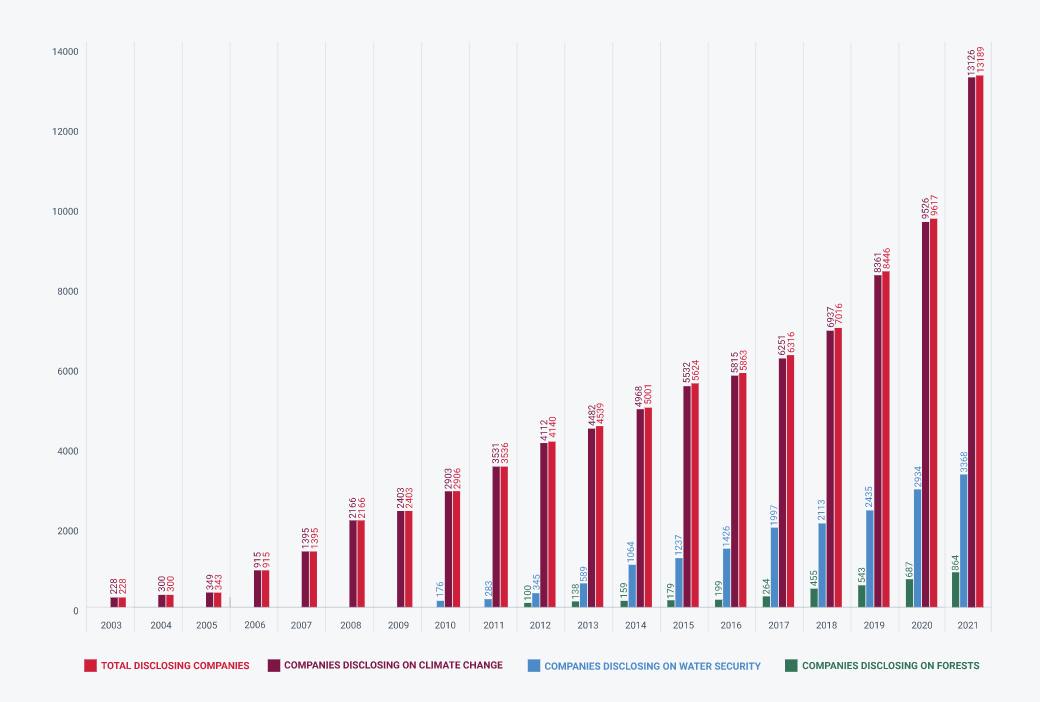

The number of companies providing their environmental impact reports by individual categories and in general continues to grow every year:

Sourse: https://www.cdp.net/en/companies/companies-scores

A company that has fulfilled at least one of the three criteria (climate change, forest restoration or water conservation) falls into a special A List, which includes all organizations leading in the field of sustainable development and representing the greatest interest for both investors and consumers.